Roadmap: Inflation then disinflation

The hottest debate in the markets right now is whether we see inflation, disinflation, or (gasp) deflation.

What’s the difference between all 3?

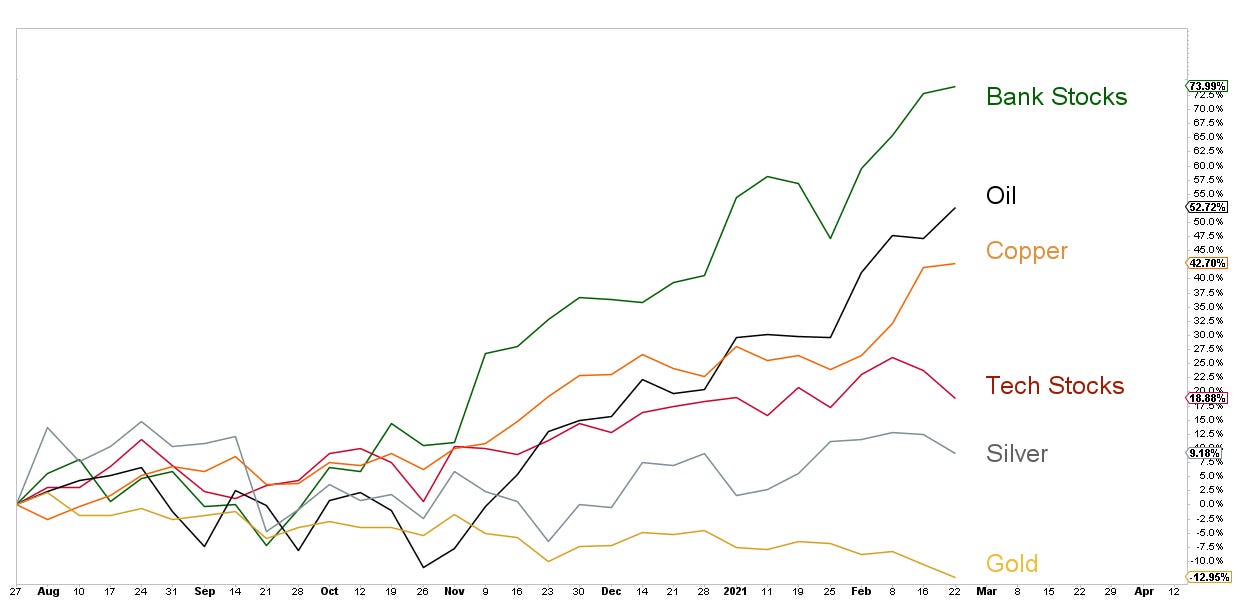

Inflation is when you have rising interest rates; commodities and stocks go up; non-US and value stocks outperform (esp. Banks, Energy, and Materials sectors); US dollar suffers. This is what we’ve been seeing for the past 4-6 months (I wrote about this here). We last had this regime during the 2003-2007 bull market.

Disinflation is when you have falling interest rates; commodities languish but stocks keep climbing; US and growth stocks outperform (esp. Tech and Consumer Discretionary sectors). This is what we’ve had for the past 10 years, as well as in the 90s.

Deflation is when you have stocks and commodities falling, but bonds rise (flight to safety). Think 2000-2002, 2008, and March 2020.

Likely scenario: Inflation then disinflation

First, the deflation scenario is highly unlikely. The Dow:Bonds Ratio monthly chart just made a 3-year breakout, after the pandemic crash retested a massive 20-yr base:

This doesn’t mean we won’t get sizeable corrections during this bull market. But the way I see it, this is a risk-on environment as I wrote in my previous post.

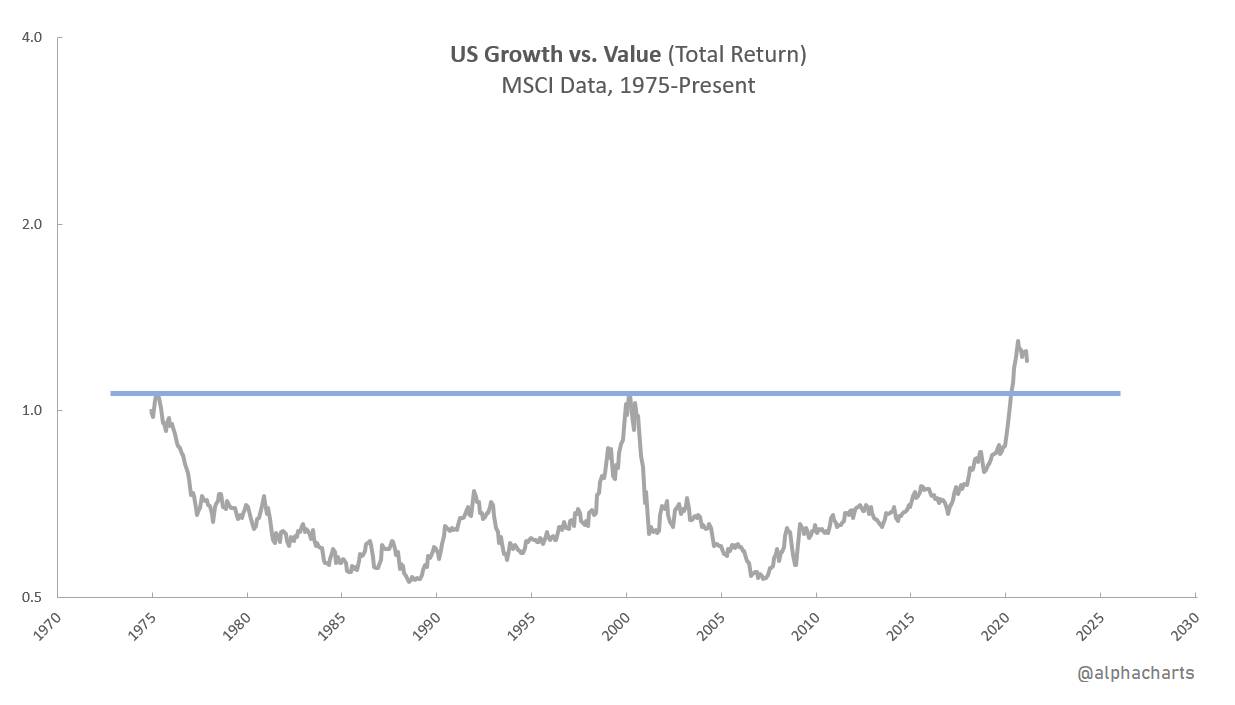

OK, now here’s a long-term monthly chart of the Growth:Value Ratio.

Growth:Value made a 50-year base breakout last year! Yes, the ratio peaked this past Nov, and we could see a retest of this base. This would mean more inflation in the months or couple years ahead, before we go back to growth outperforming like it has for the past 10 years (disinflation).

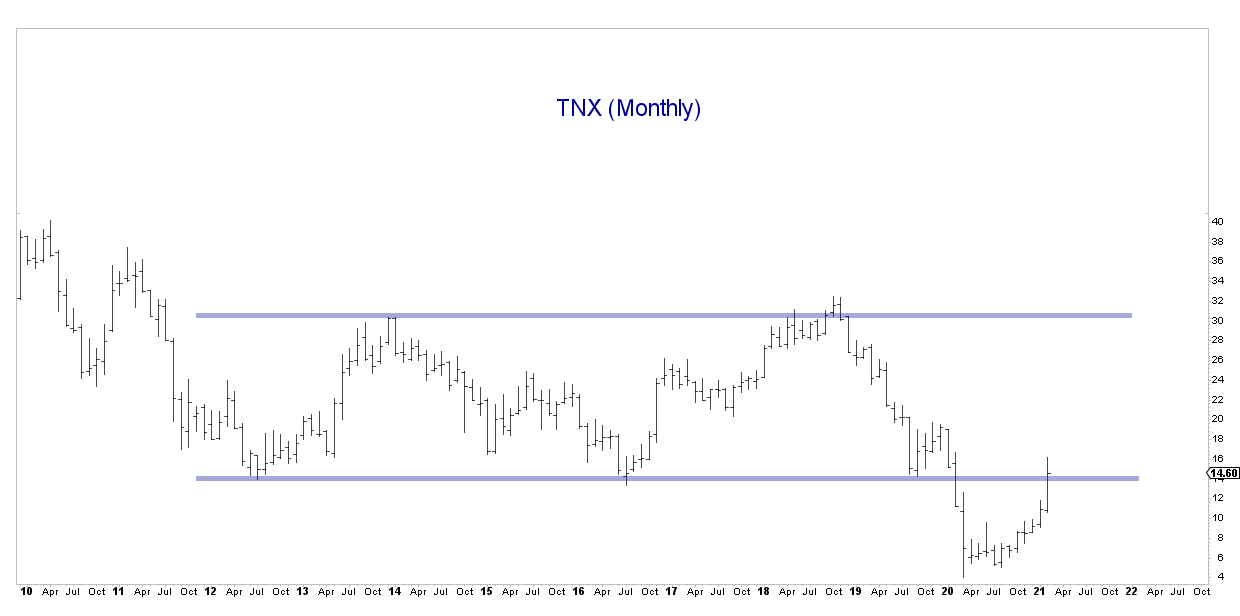

TNX Monthly. The US 10-year Treasury Yield has cleared an almost a decade-long resistance line. It can rally to as high as 3%, which is the upper-end of a 10-year range. Again, this means more inflation in the months or couple years ahead.

Yield Curve (10yr - 2yr Treasury Yield Spread). TNX has been rising while 2yr yields have been flat. This has resulted in the yield curve steepening. This spread can hit 30-year channel resistance, which again, implies 3% for TNX.

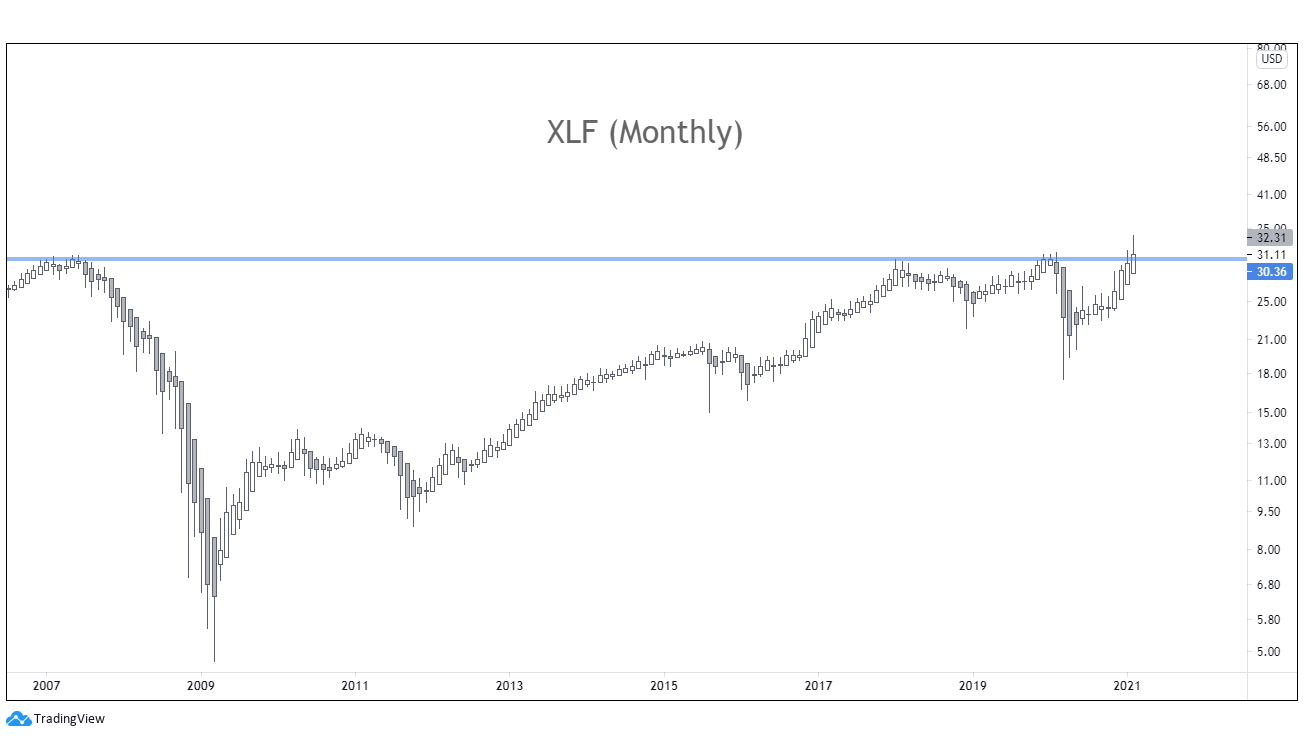

XLF Monthly. Financials have just come out of a 14-year base and have strong relative strength. Consistent with rates going higher, and Growth:Value falling, it is likely that banks maintain their momentum for some time.

A great, diversified place to park is in Canada. Like financials, the EWC Monthly chart has also come out of a giant 14-year base.

Banks, oil, materials make up almost two-thirds of the EWC ETF. The largest holding is Shopify at 8% (some tech exposure helps reduce the volatility with being very concentrated in value). Americans also get the added boost of CAD/USD exposure, which rises in an inflationary environment.

Again, given that banks and countries like Canada are just now coming out of long bases, it is unlikely we see deflation anytime soon.

Where does gold fit into all this analysis?

Like industrial commodities, gold benefits from rising inflation. However, gold also gets hurt by rising interest rates like bonds. It also tends to perform poorly when stocks are in a bull market (see this previous post). Silver should outperform gold as it has industrial uses, but I continue to avoid both. All this is consistent with the relative strength since last August.

Thoughts from smart investors

3-weeks ago, I wrote this post summarizing what Stan Druckenmiller said in a recent interview. First, Stan acknowledged that this is the most difficult that it’s ever been to make a roadmap for the markets. He then went on to say how he is positioned for inflation (short bonds & USD, long commodities & emerging markets). Longer-term, he is very bullish on tech.

Star growth manager Cathie Wood recently gave some awesome commentary:

Cathie believes that the 10yr yield can climb to as high as 3% and top out there (consistent with the chart analysis from above). She also mentions that she’s happy to see value outperforming here as it’s healthy for the broader market. This is the right mindset. Looking at the Growth:Value chart above, it’s healthy for a strong uptrend to have pauses/consolidations. This washes out sentiment and gives energy for each successive leg higher.

Cathie believes that rates then eventually start coming back down and growth begins outperforming again for 2 main reasons:

Tech innovation (“good deflation”)

Disruption of old economy companies, many of which are highly leveraged (“bad deflation”)

Cathie mentions that innovation is accelerating. Vanguard has done a lot of research on what they call The Idea Multiplier, and have come to a similar conclusion: the next 5yrs will have twice the productivity growth as previous 2 decades. You can find this research here.

The pace of innovation is something we can easily take for granted. But many tech companies, the smartphone, the cloud, gene editing, and the blockchain weren’t around 20 years ago.

Up until just 10-15 years ago, image & voice recognition were the biggest hurdles in computer engineering. While machines could run laps on humans when it came to basic arithmetic, humans had the advantage when it came to recognizing a person in a crowd or specific sound.

Then suddenly, that problem was solved with ML/AI. Its result? Voice assistants, autonomous vehicles, advanced robotics, etc. These tools are just starting to be adopted in every industry, including mineral exploration, manufacturing, genetics, finance.

These discoveries all build on top of each other to produce exponential growth.

Of course, this last section of my post is full of opinions/narratives. But they are inline with what the long-term charts show us. We always want to be aligned with the trend.

“Strong opinions loosely held.”

Important Disclaimer: This blog is for educational purposes only. I am not a financial advisor and nothing I post is investment advice. The securities I discuss are considered highly risky so do your own due diligence.